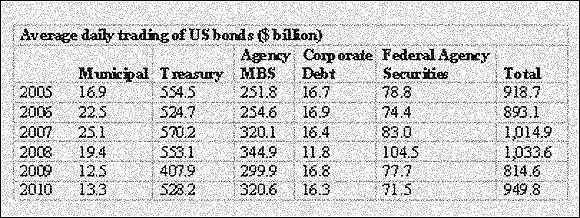

MBS = mortgage backed securities

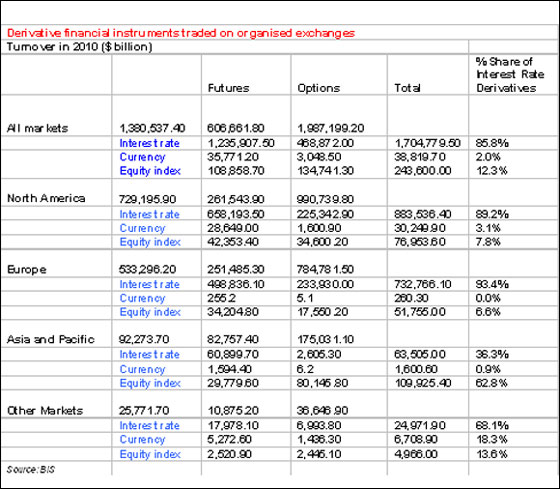

It is just the same with financial derivatives. According to the Bank for International Settlements (BIS), interest rate derivatives accounted for over 85 per cent of the total notional derivatives turnover on organised exchanges.

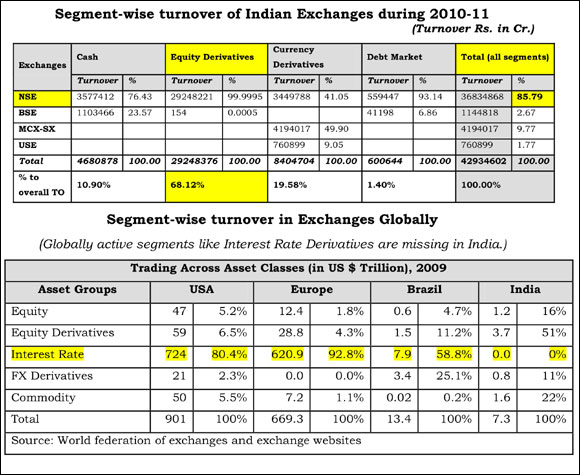

Yet this segment has failed to take off in India (see table on derivative financial instruments traded on organized exchanges).

Will the MCX-SX (Multi-Commodity Exchange - Stock Exchange) be able to make a difference in this pattern of trading in different categories of financial instruments?

It will, of course, offer asset classes such as equities and equities F&O, interest rate futures and wholesale debt segments. A lot more is expected of MCX-SX in terms of rejuvenating the equities space in the country though.

On the cards could be lower transaction costs to attract brokers. Such incentives can be supplemented by innovative and technology-driven schemes, efforts to make markets for mid-cap shares to boost liquidity and a focus on the space for trading in financial instruments of MSMEs.

Why is the MSME sector important for India and the equities market? It is because micro, small and medium enterprises sector dominate the Indian economy, accounting for more than 90 per cent of the enterprises in the country.

The labour intensity in the MSME sector is estimated to be almost four times higher than in large enterprises.

Click on NEXT for more...

Nobody really knows the exact number of MSMEs in India. The official website of the government of India's Ministry of Micro, Small and Medium Enterprises places the total number of MSMEs at 26.1 million at the end of March 2007 that together employed 59.7 million people.

However, according to the final report of the 4th Census of the MSME sector released in April 2011, there were just over 1.514 million "perennial" MSMEs in India employing nearly one million people in 2006-07.

This sector accounts for about 45 per cent of the value of the country's manufacturing output and around 40 per cent of total exports. SMEs alone produce more than 8,000 products for the Indian and international markets.

This sector, accounting for 17 per cent of India's gross domestic product in 2011, is afflicted by a host of problems. Important among these is the problem of financial exclusion.

The reasons why capital markets are important for MSMEs are well known and worth recounting:

Click on NEXT for more...

A question may well be asked as to why existing stock exchanges have not and are still not fulfilling the role of assisting MSMEs. In September 2011, Sebi granted approval to the BSE to start a trading platform for MSMEs and the following month, a similar approval was granted to the NSE.

A rejuvenated Calcutta Stock Exchange was supposed to be dedicated to stocks of small firms. Nothing noteworthy has happened on these fronts.

Surely the main problems relating to deepening India's capital markets - in terms of getting more people to participate in investment and trading in equity shares and other financial instruments - lies in the governance of the Indian corporate sector (be it companies in the public sector, the private sector or multinational corporations), disciplining dominant shareholders or promoters and in protecting the interests of minority shareholders.

An NSE spokesperson said that the bourse dealt with investor complaints with alacrity. Of the 6,131 complaints received between August 2011 and August 2012, the NSE resolved 5321 complaints (79 per cent) and the others are in various stages of resolution.

More importantly, the NSE says that it holds an average of 1,300 investor seminars every year to create awareness on the 'dos' and 'don'ts' of trading. Yet issues remain about the general state of corporate governance in India.

Click on NEXT for more...

How will the advent of the MCX-SX help improve corporate governance? A source close to MCX-SX, speaking on condition of anonymity, argues that India's capital markets are not being fully tapped to raise risk capital or geared for "real" capital formation and wealth distribution.

There is immense scope to develop a wide array of financial instruments for risk management, savings and investments across the value chain, risk horizons and yield curves thereby shifting investor preferences away from equities.

The source says the "need of the hour is to make available the entire range of financial products to all citizens for capital mobilization".

Diverse financial service providers along with enhanced competition in the capital markets will foster innovation, he contends, adding that making available a variety of financial products to all citizens and encouraging participation in all these product segments by raising investor awareness, education, technology innovation, improving service levels and cost optimisation will eventually lead to "inclusiveness in our financial markets" .

Click on NEXT for more...

He believes it is not the lack of regulation that is preventing broad-basing of investors in India but lack of focus, competition and innovation among providers of financial products and services.

Clarification:

In the first part of this article it was written that the "NSE is mutually owned by a clutch of leading financial institutions, banks and other financial intermediaries, including at least two foreign investors, NYSE Euronext and Goldman Sachs."

A spokesperson of NSE has clarified that NYSE Euronext exited from the NSE nearly two years ago. Global shareholders of the NSE currently include General Atlantic Investments, Goldman Sachs, Citigroup, Morgan Stanley (all through their investment arms in Mauritius), Tiger Global Five Holdings and Aranda Investments (which is part of Singapore's Temasek group).

The error is regretted.