Even as most global leaders were affected by an economic slowdown, Indian markets scaled new highs in 2014, thanks to the optimism about a stable govt at the Centre, a demand revival and falling oil prices

BSE Sensex, year of many highs

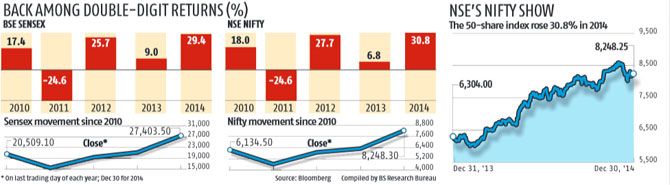

For the Indian equity market, 2014 was a year of many highs.

The BSE Sensex, which hit an all-time high on the first trading day of the year, clocked new life-time closing highs in more than 50 trading sessions during 2014, underscoring the secular upward trend the benchmark index had seen.

Leaving behind an uncertain start to an election year, the bulls took charge in mid-February, at a time when the Sensex had dropped to 20,193.

The beginning of the surge coincided with Arvind Kejriwal stepping down as Delhi’s chief minister and the general election campaign of the Bharatiya Janata Party’s prime ministerial candidate Narendra Modi picking up steam.

Even before India went to polls in April, the market had gained a little more than 12 per cent from its lows, on the hope of a favourable election outcome. The rally gained pace as exit polls suggested BJP might come to power at the Centre. A day before the historic election results, the Sensex had risen 18 per cent from its February lows and was nearing 24,000.

The market’s optimism was vindicated, with the Modi-led BJP getting the most decisive mandate in 30 years, and there was a further upmove when Modi became India’s 15th prime minister. There was an across-the-board surge, and even the beaten-down sectors like real estate, infrastructure and power gained sharply in anticipation of a reform push by the new government.

The market’s optimism was vindicated, with the Modi-led BJP getting the most decisive mandate in 30 years, and there was a further upmove when Modi became India’s 15th prime minister. There was an across-the-board surge, and even the beaten-down sectors like real estate, infrastructure and power gained sharply in anticipation of a reform push by the new government.

A robust risk appetite among global investors, amid loose monetary policy stance of global central banks, including the US Federal Reserve, the European Central Bank (ECB) and the Bank of Japan, added to the gains.

A set of early reforms, including the deregulation of diesel prices and opening of the mining sector, and an improvement in macroeconomic metrics, further charged the market.

The stock market’s 2014 journey was mostly turbulence-free, save for two instances. First, there was a drop of about five per cent in October, on concerns the US Fed might advance its interest-rate increase. And second, a sharper correction in December — of around seven per cent from an all-time high of 28,693 touched on November 28 — amid falling crude oil prices and troubles faced by the Russian economy. Foreign flows, which had reached a peak of $17.4 billion, saw some repatriation.

Another interesting trend that emerged this year was that domestic institutions, including mutual funds and insurance companies, stepped up buying whenever there was selling by FIIs. Analysts expect equity MFs, which have received nearly Rs 30,000 crore (Rs 300 billion) of inflows since May, to emerge as key buyers next year.

On the flip side, the Indian market, having posted its biggest annual gain since 2009, faces headwinds in the form of slowing foreign flows and a global economic slowdown. Also, expensive valuations provide less legroom for the market to move up sharply from its current level.

India vs World

Outperforming all, except China

Indian markets outperformed their peers in most other emerging and developed markets during 2014.

Thanks to a drop in global crude oil prices and exuberance around a stable government coming to power at the Centre, the year was the best one since 2009 for the country’s markets.

Among Brics economies, China was the only country whose stock market outperformed Indian benchmark indices. China’s surge, though, began only around June and many commentators questioned the basis for the rally, arguing there was no noteworthychange infundamentals.

By comparison, the surge in Indian indices was not without fundamental support. While the rest of the world was dealing with an economic slowdown, India saw the fewest earning downgrades among Brics nations. Brazil and Russia, meanwhile, were affected by falling commodity prices and geopolitical issues, in addition to the fears of a 'hard-landing' in China.

Analysts also expect the rate of earning growth in India to be higher than elsewhere in the world. Over the next two years, the country’s earnings are expected to grow at 16 per cent - higher than China, the US, UK and Japan among major economies — according to a Credit Suisse India Market Strategy report dated December 8.

In this environment, India stands out as a rare economy with relatively strong growth. Despite the (marginal)pick-up in forecast for global growth in 2015, the growth gap between India and the world is expected to widen,” said the Credit Suisse report, authored by research analysts Neelkanth Mishra and Ravi Shankar.

Sectoral indices

A demand-driven story

The consumer durables sector was the best performer this year, as investors bet on an improvement in the demand scenario.

The expectations of the Reserve Bank of India (RBI)moving closer to lowering the interest rate helped whet appetite for the consumption story. The belief that a lower interest rate would make it easier for consumers to purchase goods aided a rally in stocks in the sector. The automobile index also did well, on the back of an improvement in sales.

The banking index was a good performer as well. It rose more than twice as much as the benchmark Sensex. This was also a sentiment booster, as banking stocks are widely seen as a proxy for the overall economy: If the economy does well, banks’ business improves and stressed assets come down.

Among the sectors that disappointed the most in 2014 was metals. The metals index trended downwards, in line with the decline in global metal prices. This was mainly on account of waning demand, as some of the major economies remained under the shadow of a slowdown.

The worst performer among BSE’s 11 sectoral indices, though, was the real estate index.

The investors who put their money in this sector would have got returns of only 5.65 per cent - much lower than most fixed deposits, which offer eight per cent or more. The real estate sector bore the brunt of anaemic sales, piling inventory and regulatory action against some of the top developers. A high level of debt on the books of top companies in the sector added to the woes.

Rupee, bonds & oil

Stable amid crude shock

The year 2014 was a relatively quiet one for the rupee, especially after suffering steep declines against the dollar the previous year.

In 2013, the rupee had moved in the range between 53.1 and 68.8 a dollar. In contrast, the Indian currency moved in the band of 58.5 to 63.6 a dollar this year. In December, though, some weakness was seen, even as most emerging-market currencies fell against the dollar on global economic worries.

The yield on government bonds, meanwhile, fell sharply this year from the level a year ago. The decline in yields was attributed to

expectations of a cut in the interest rate by the Reserve Bank of India, on the back of softening inflation numbers.

The yield on the benchmark 10-year bond dropped below eight per cent, compared with 8.83 per cent at the end of last year.

For crude oil, however, it was a historic year. After remaining steady above the $100-a-barrel mark for much of 2014, the global oil prices came crashing down towards the end of the year. Fears of oversupply saw the commodity, often referred to as black gold, declining nearly 50 per cent from its June high of $115 a barrel. A drop in demand from key markets like China and Japan, and the Organization of the Petroleum Exporting Countries’ refusal to reduce production contributed to the drop.