The Securities Contract Regulation Act (SCRA) was amended in December 1999 to include derivatives within the definition of securities.

The passage of this Act made derivatives legal as long as they were traded on a recognized stock exchange. Exchange Traded Financial Derivatives were introduced in India, in June 2000, on the National Stock Exchange and the Bombay Stock Exchange.

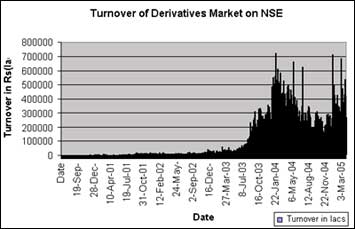

The beginning was made with index futures contracts based on S&P CNX Nifty Index (Nifty) and BSE Sensitive Index (Sensex). Since then, the rise in the turnover of derivative contracts traded on NSE has been exponential (See graph, data source: www.nseindia.com).

It is worth mentioning here that NSE has around 99.5% of the market share of exchange traded financial derivatives market in India.

Stock futures and Index futures are two of the most popular contracts traded on NSE, having a market share of 59% and 29% (by turnover) respectively of the total derivatives market segment. In this article, we will concentrate on the trading mechanism of the futures contracts.

Trading mechanism of futures contracts

A futures contract gives the holder the right and the obligation to buy or sell the underlying at a certain price upon maturity. The underlying in case of a financial futures contract can either be an index or the stock of an individual company.

(For further details refer to our article All you wanted to know about derivatives!)

A futures contract, whose underlying is the stock of an individual company, is known as stock futures. Similarly, if the underlying is a stock market index, the contract is known as an Index Futures contract.

Let us understand futures trading with the help of an investor (say, Mr Bull) who is of the opinion that the stock market will go up in the days to come. He wants to take advantage of this.

The market is represented by an index. An index constitutes of various stocks from different sectors that trade in the market. Each stock has a certain weightage in the index and depending on the movement of these stocks the index moves up or goes down.

To cash in on the rising markets, Mr Bull can invest in stocks that constitute the index in a proportion that is equivalent to their proportion in the index. However, investing in all the member companies of the Index will be a very expensive and a time consuming process.

The alternative is to invest in Index futures. So Mr Bull decides to invest in Nifty futures. Let us say that Nifty is currently at 2,000 mark. Mr Bull gets into a futures contract, expiring on August 25, 2005, to buy 200 units (The permitted lot size of Nifty futures contracts is 200 and multiples thereof) of Nifty Index at Rs 2,010.

Let us say that the initial margin that the investor needs to pay is 10%. Thus, the initial investment is only 10% of 200 times 2,010 (Rs 4.02 lakh, the value of the contract); which is Rs 40,200.

For any market to work, every buyer needs a seller. So the other side of the coin is an investor (say Mr Bear), who believes that the market will go down in the days to come. Mr Bear gets into a futures contract, expiring on August 25, 2005, to sell 200 units of the Nifty index at Rs 2,010. The seller also has to pay an initial margin of 10%, hence his initial investment is also 10% of 200 times 2,010; which is Rs 40,200.

Before we go any further, we will need to understand an important feature of futures contracts, Mark-to-Market (MTM). MTM is a fancy term used for adjusting the value of an investor's investment on a daily basis.

This means that the difference between the settlement price (the closing price of the futures contract) of the previous day and the settlement price of today is settled in cash daily. Any gain or loss made by the investor on a day has to be settled in cash.

Taking the example further, let us look at the table below to see how MTM works:

Table 1: Mark-to-Market (From Mr Bull's perspective)

|

Day |

Exercise Price |

Daily Closing Price of Index futures |

Difference to be (paid)/received in cash |

Notes |

|

1 |

2010 |

2000 |

-10 |

On the first day, gain or loss is calculated as the difference between the Exercise Price and the Settlement price (The Closing Price of the futures contract). |

|

2 |

|

2025 |

25 |

From the second day onwards, the gain or loss is calculated as the difference between previous day's settlement price and today's settlement price. |

|

3 |

|

2030 |

5 |

|

|

4 |

|

: |

: |

|

|

5 |

|

: |

: |

|

|

: |

|

: |

: |

|

|

: |

|

2010 |

: |

|

|

Expiration day |

|

|

70 |

On the expiration date, the final settlement is the difference between previous day's settlement price and the spot price (Spot Price is the current market price of the underlying at any point in time) of the underlying. In this example, the spot price of the index is Rs 2,080 on expiration date. |

In the above example, on the first day, the settlement price is 2000, so Mr Bull will have to pay Rs 10 per of contract (Rs 2,000 - Rs 2,010) i.e. a total of Rs 2,000 for 200 contracts to the exchange.

The exchange in turn passes on this money to Mr Bear, who holds an opposite contract and thus has made a profit. On the second day of the futures contract, the settlement price is Rs 2,025. So Mr Bull in this case gains Rs 25 (Rs 2,025 Rs 2,000) per contract, i.e. a total of Rs 5,000 for 200 units of contract.

In this case Mr Bear has to pay Rs 5,000 to exchange which will be passed onto Mr Bull. All this settlement is done with the help of intermediaries (known as Clearing Members).

In India, all the exchange traded financial derivatives are cash settled. This is because physical delivery would be highly inconvenient or impossible. For example, in the case of an index futures contract, physical delivery would mean delivering the shares of the components of the index, in the weights that it placed on them in calculating the index.

Also, it would involve enormous amount of regulatory and administrative formalities.

Upon the expiration of the contract, a final settlement is made where the investor gets back his initial margin, along with the gain or loss on the last day.

The gain or loss on the last day is calculated as the difference between the previous day's settlement price and the spot price of the underlying (in this case the index) in the cash market.

Now suppose upon the expiry of the contract on August 25th, the index is at the 2,080 mark. Mr Bull will receive his initial deposit of Rs 40,200 plus the gain on the futures contract. The gain will be (2,080-2,010)*200 units, i.e. Rs 14,000.

There are some brokerages charges to be paid for trading in futures contracts, which are 2.5% of the contract value. Thus the net gain will be Rs 14,000 less 2.5% of Rs 4,02,000 (Rs 10,050). The profit for Mr Bull will be Rs 3,950 (Rs 14,000 Rs 10,050). The return is 9.8% on the investment of Rs 40, 200 for Mr Bull.

Now look at Mr Bear. For him, the losses far exceed the gains made my Mr Bull. Mr Bear not only has to bear a loss of Rs 14,000 due to the movement of index in direction opposite to his expectations, but he also has to pay the brokerage charges.

The brokerage charges are once again 2.5% of the contract value (which is Rs 10,050). Hence the total loss for Mr Bear is Rs 24,050 (Rs 14,000 + Rs 10,050). A loss of 59.8% on an investment of Rs 40,200.

This is the reason why derivatives are considered very risky investments. While there are opportunities to get higher returns, the losses can far exceed the gains if the strategy goes wrong.

At present individual stock futures contracts are offered on 87 stocks. Investments in stock futures contracts work in similar way as the index futures.

Conclusion

In this article, we have tried to look at exchange traded financial futures contracts as a tool of investment. The popularity of futures contracts in India is contrary to the trend in other parts of the world, where option contracts are more popular than the futures contracts.

We think that one reason behind options not picking up in India could be because options are more complicated to trade in. With this in mind, we will devote our next article to simplifying options trading for our readers.

DON'T MISS:

Nupur Hetamsaria is Visiting Research Scholar, Syracuse University, NY; and Vivek Kaul is a freelance writer.