For long, currency and bank deposits have grown together. Inflation, nominal interest rates hold the key to why they are no longer doing so, rues Arvind Subramanian

For long, currency and bank deposits have grown together. Inflation, nominal interest rates hold the key to why they are no longer doing so, rues Arvind Subramanian

Two puzzling monetary developments have recently attracted considerable attention -- the slowdown in bank deposits and the acceleration of currency in circulation.

Are these two developments related?

In particular, is it plausible that both currency acceleration and deposit deceleration are due to imminent elections?

In fact, the real story seems more complex, and has important implications.

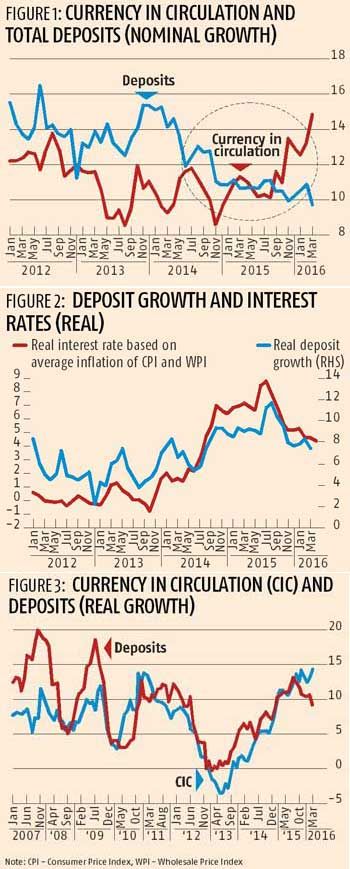

Figure 1 illustrates the puzzles. It shows that nominal deposit growth has declined from a high of 13.1 per cent in August 2014 to 9.7 per cent in March 2016.

Meanwhile, currency growth has accelerated from 8.5 per cent in November 2014 to 14.9 per cent today.

Before explaining these developments, an important technical point must be highlighted.

Almost all the recent commentary overlooks the fact that at a time of rapid price changes nominal magnitudes can be misleading.

The focus must, therefore, be on real magnitudes.

Consider, then, real deposit growth, which is plotted in Figure 2.

From it, four facts emerge that explain the deposit puzzle.

First, the real aggregates move differently from nominal aggregates: for most of 2015 the decline in nominal deposit growth was offset by falling inflation so that real deposit growth was in fact accelerating.

Second, since late 2015 real deposit growth has indeed been plummeting, from about 11.7 per cent in August 2015 to 7.4 per cent most recently.

Third, even so, the current rate of deposit growth is not particularly slow.

It seems that the recent deceleration actually represents a reversion to the mean; in other words, it was the high and accelerating deposit growth in the period September 2014 to August 2015 that was unusual, rather than the deceleration more recently.

Fourth, this behaviour seems to be well explained by changes in the real deposit rate, the return that savers get for putting their money in bank deposits.

The correlation between real interest rates and deposit growth is strikingly tight, suggesting a connection between the two.

Essentially, after a period of high inflation when people’s confidence in money declined, funds returned to the banking system when savers were rewarded with positive real returns.

After this transitional period (September 2013 to July 2015), we are now witnessing a more normal phase, with healthy real deposit growth of seven per cent.

This analysis suggests that slower deposit growth should not be ascribed to slower income or gross domestic product growth as Harish Damodaran of The Indian Express recently contended: the key driver of deposits is really lower real interest rates, and in any case the level of real deposit growth is not worryingly low — it is actually higher than in recent years.

Consider next the currency puzzle. Figure 1 suggested there has recently been an exceptional surge in currency in circulation.

But as with deposits, this impression is misleading, because it fails to take prices into account.

Figure 3 shows that developments in real holdings of currency paint a very different picture.

Once again, it was actually the high inflation period -- which led to a drop in currency growth -- that was anomalous.

Correspondingly, the recent acceleration appears to be a return to trend.

For this reason, and because there is no marked blip up in currency growth in the run-up to the general election in May 2014 (and indeed there are a number of blips in non-election periods as Figure 3 shows), it seems less plausible that state elections are responsible for the recent acceleration in currency growth.

But there is still the question of why currency growth and deposit growth, which moved together for such a long time, have suddenly decoupled.

One explanation could be that when inflation went up both currency and deposits were relatively less attractive to hold, but as inflation has stabilised, and nominal interest rates have come down, currency has become more attractive relative to bank deposits.

Several important implications follow from this analysis.

If the slowdown in deposits continues, banks could remain under tight pressure for resources.

In this case, banks will have less scope to lend, and the current credit slowdown will intensify.

Banks will also have less room to reduce lending rates, thereby impairing monetary transmission. All of this will also affect real activity.

How should the Reserve Bank of India respond to these risks?

How should the Reserve Bank of India respond to these risks?

It will need to monitor liquidity in the banking system carefully, and react quickly if problems arise.

In particular, the RBI will need to fulfil its April 4 pledge to avoid liquidity shortages.

In the five months prior to the Monetary Policy Statement, the liquidity shortage -- documented in the Economic Survey -- had kept banks under severe stress, hampering the overall economic recovery.

That experience should not be allowed to recur as the environment gets more challenging.

Arvind Subramanian is chief economic advisor, Ministry of Finance, government of India