The world is alive with the sound of inflation. Policy makers are troubled and central banks have retreated somewhat from their lofty one-shoe-fits-all (read inflation targeting) policy they were trumpeting not so long ago. There are no easy solutions in sight, just speculation about policy response.

We are all running helter-skelter to answer the big question - not the sub-prime crisis, or banks going bust, or even whether the US is, or will be, in a recession.

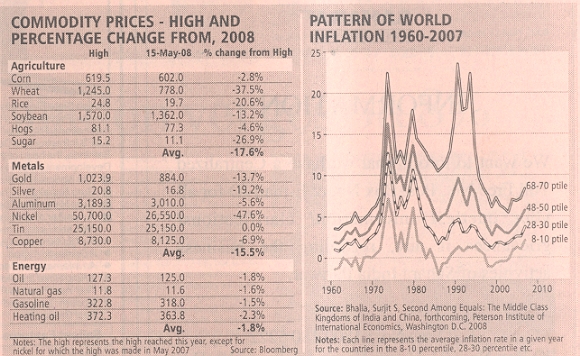

Quite simply, the need is for an assessment of the future course of inflation. An examination of the past may be the first pointer. The graph shows averages of country-level inflation since 1960 with countries bunched according to their rank in each individual year.

For example, Brazil was a member of the hyper-inflation club in 1990 (rank of 99) and an above-average performer in 2007 (rank of 38). The results are striking - the pattern of inflation change was not a function of inflation targeting, or even whether a country had a central bank or not!

Low inflation in the 1960s, peak inflation in the mid 1970s and early 1980s (the oil and wheat shock of 1972/73 and the oil shock of 1979); and a large structural decline since 1980 with a trough in the early 2000s.

Last few years, practically all countries show an acceleration in inflation. Inflation targeting or reducing/anchoring inflationary expectations did not play much role in reducing inflation; if not, what did?

Most likely, the prime cause has been the important role of productivity growth in developing countries, especially the large-sized countries like China and India. With Africa and Latin America now joining the development party, subdued world inflation is more likely than not.

It might be news to George Bush, but this productivity and income growth did lead to more demand for food and commodities and oil in the developing countries over the last not one, not five but last 20 years. During the same period, however, commodity prices generally declined, or worst case, stayed constant in real terms.

But what happened to the forecast of low inflation in 2008? World inflation is broadly composed of three commodities: energy, agriculture and metals (both precious and other metals). The long-term pattern of commodity inflation is as follows.

A trough in 1997/98 (Asian crisis), and then a rise such that by late 2007, real commodity prices were on their highs but still considerably below the peak reached in the 1980s. Simultaneously, world per capita growth exceeded 3.5 per cent per annum (purchasing power parity data) during these years - a level not seen since the 1960s. So the pattern, until 2008, has been of high economic growth, high increase in commodity prices and low individual country inflation!

So what did happen? A reasonable speculation is that this recent burst in prices has more to do with old-fashioned speculation than even older-fashioned fundamentals. In this regard, the recent hysteria pertaining to the Indian rupee is relevant. Then (was it just a month ago?) the slogan was: India is a fast-growing country, currencies of such appreciate, and therefore the rupee should go to 38/US$ by June 2008.

Today, the rupee is at 42.8/US$. The same explanation (story) is forwarded for commodities; India and China are growing, so demand will grow etc. etc. Just like gravity had to catch up with the rupee (notwithstanding the well grounded in fundamentals forecast of all the major investment banks, domestic and international), so is gravity likely to catch up with commodity price inflation.

Trends in world inflation will likely dictate domestic inflation. Except for oil, the major commodities of the world are already in a downward slide. The attached table tells the story.

First, agricultural commodities (the source of the political problem with inflation) have already declined (from their peaks made just weeks ago) by significant amounts. As of May 16, wheat prices are off 39 per cent; soybean prices (for edible oils) are off 13 per cent.

Even rice prices, after catapulting just a few days ago, are off 16 per cent. On average, food prices are off 15 per cent from their highs. The same magnitude of decline is witnessed in the metals space, precious or otherwise.

But what about the price of oil? The oil complex remains at its highs; after making a new high just a few days ago, the oil complex is off 2 to 4 per cent, i.e. no decline. The present oil price is some 20 per cent higher than its highest real price, ever. If one adds the value of the dollar (up 3 to 10 per cent from the lows against major currencies) then oil remains the only glaring exception in the commodity space.

In this regard, it is pertinent to note that the Dow Jones Transportation average is up 17 per cent for the year - just slightly less than the increase in the price of oil! If other commodities are any guide, then the identity of which market is smoking what will soon be known.

When international commodity prices come down, domestic inflation will also come down. There is very little demand pull left in India; the monetary authorities have achieved their objective (right or wrong) of considerably slowing down the economy.

Wage growth, an indicator of demand pull inflation, is barely keeping pace with inflation; bank credit growth has also slowed down drastically; and real interest rates are among the highest in the world. And until very recently, our exchange rate had also appreciated close to the maximum in the developing world.

None of this was successful in insulating India from importing world inflation; indeed, our acceleration of inflation, while lower than China, has been on the high side in the developing world. So India has lost out both in terms of lower economic growth and higher inflation.

What is the appropriate policy response to this inflation? Patience. Inflation will likely decline, and by fall 2008, the world (and domestic) inflation could be stable, and lower. Growth should also be accelerating at that time.

Better for Indian policymakers to step back from the brink, say that they are doing everything that is advisable and possible, and let prices unfold. And plan for elections in the winter!

The author is Chairman, Oxus Investments, a New Delhi based asset management company. The views expressed are personal.