India's corporate sector has taken up the challenge of making overseas acquisitions of over a billion dollars and also to make mega investments in the country. The latest Economic Survey says an investment of $150 bn is required from the private sector in physical infrastructure alone to sustain a 9 per cent growth. It further states (Para 9.136), "There is a lack of availability of risk capital to support debt coupled with inadequate flow of equity capital into infrastructure."

India also competes with the BRIC and ASEAN economies for foreign investments. Does the Indian entrepreneur get a supportive fiscal and banking environment to meet the challenges? Does the tax on inter-corporate dividend (whether from domestic companies or foreign companies), facilitate capital formation?

A domestic company pays dividend from its income after tax. The payer subjects this dividend to a dividend distribution tax at 17 per cent, which is nothing but a sophisticated substitute for tax at source and is not taxed in the hands of the recipient again. When an investor company pays dividend out of this dividend, it has to again pay Dividend Distribution Tax (DDT), thus amounting to triple taxation of the same income.

Such double and triple taxation is against all principles of equity. In India it seriously impedes capital formation also. The effective cost of paying a 20 per cent dividend increases to 23.4 per cent at each stage.

Corporates tend to reduce dividend payouts. The recipient company's dividend value further falls due to DDT on that company. The Budget speech 2008 acknowledges this: "As a result, the distributed dividend is sometimes taxed twice in the hands of a subsidiary company and its parent company, causing hardship".

Finance Minister P Chidambaram has proposed one exception to the DDT where the recipient company is a holding company having 50.1 per cent of the shares of the paying company; and the recipient company is not itself the subsidiary of another company, it would not again have to pay DDT. Inter-corporate investment plays a critical role in stimulating economic growth, and more importantly, of encouraging capable entrepreneurs to grow into mega size.

Having recognised the need for an efficient structure and removal of the cascading impact, only a half-hearted relief is proposed. But the implication of such cascading taxation is far more deleterious to growth than simply a tax of 17 per cent.

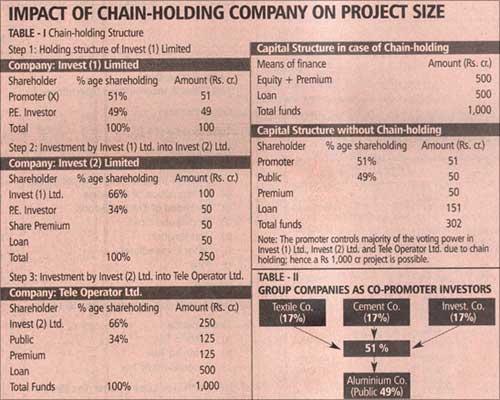

Both infrastructure and industry demand huge investments, especially as promoter contribution. These require flexible holding structures. At different forums, Chidambaram has stated that (a) he is not convinced about the need for chain holding companies; and (b) circular investment companies are merely tax-avoidance devices. Some examples will put the issues in the correct perspective.

A chain of two or three investment companies becomes necessary to raise promoter funding, as is clear from Table I. A promoter with management and project skills, but with limited resources, is able to leverage his funds so as to raise the large fund required to promote and control even Rs 1,000 crore (Rs 10 billion) projects with Rs 50 crore (Rs 500 million) of investment.

The telecom sector's growth is adequate proof of this. The private equity (PE) player must gain confidence in the business model and in the promoter for the success of a chain-holding model. Such PE investments are raised at a premium. The total capital is then leveraged to raise loans in the investment company depending on its expected cash flow from dividends.

An investor putting in Rs 51 crore (Rs 510 million) is able to leverage equity funds of Rs 500 crore (Rs 5 billion), raise loans of Rs 500 crore and put up a project of Rs 1,000 crore (Rs 10 billion) in a chain-holding structure as against only Rs 302 crore (Rs 3.02 billion) in a directly promoted Tele Operator Ltd.

Due to DDT, which has a cascading impact, the cash flows reduce and hence value of each chain investor company reduces by 17 per cent at each level. It thus reduces the leveraging capability for raising equity at a premium or loans as cash flow for repaying loans reduces.

In the chain-holding structure example, DDT is paid three times - once in Tele Operator Limited; second in Invest (2) Limited and third in Invest (1) Limited amounting to an aggregate of 51 per cent. Alternatively, if Tele Operator Limited is a subsidiary of Invest (2) Limited and Invest (2) Limited was not a subsidiary of any other company, there would have been only 17 per cent DDT at the level of Tele Operator Limited only. It is the absence of such a facilitative environment in India that has led to the creating of such structures abroad for investment into India.

SPVs for foreign takeovers also need to be encouraged in India. For example, Tata and Hindalco had to create an SPV abroad to fund the takeover of Corus and Novelis because, inter alia, (a) dividend income received from foreign companies into India suffers tax at 33 per cent or at the rates prescribed in the Double Tax Avoidance Agreements with respective countries or at full rates; and (b) such SPVs cannot be listed on foreign stock exchanges without being listed in a stock exchange in India.

Such an SPV in India could have utilised India's forex resources also; and all dividends would have flown back to India rather than being parked abroad.

The second model of raising promoter finance is where three or four companies of the same group pool investible resources. This also spreads the risk of new investments. Table II depicts this fairly common model. If only the Textile Co were to hold 51 per cent of the Aluminium Co, then the Textile Co would get relevant exemption from dividend distribution tax; but where investment is only 17 per cent, this exemption will be withdrawn.

Does this promote large capital formation and large projects or would each investor be forced to take up medium-scale projects only where it can hold 51 per cent equity?

In a third and successful model which is practised abroad, promoters fund the nucleus capital of investment corporations; then float them on the stock exchanges; public capital is raised; and provided as equity capital to many companies in diverse industries.

Such investment companies should really be seen as pass-through vehicles like mutual funds dedicated to equity investments.

They suffer DDT, short-term capital gains tax at 15 per cent or on share sale profits at 33 per cent; and interest on loans taken for such investments is not deductible as dividend is not taxed.

Flexible structures are required in large infrastructure construction projects where consortiums are formed or in real estate business due to land ceiling. This regime is also discriminatory when compared to many foreign companies investing into and receiving dividend income from Indian companies without suffering DDT on their own dividend declaration.

The system of DDT also reduces India's competitiveness for attracting inward foreign investment vis-a-vis other countries. DDT, though essentially a tax on dividend and a substitute for withholding tax, is not available to foreign companies in their countries of domicile as tax credit against tax on dividend income which they receive from Indian companies.

Perhaps, a suitable deeming provision could be brought in to Income Tax Act to state that DDT would be deemed to be income tax on dividend in the hands of the foreign company.

The finance minister has stated that circular holding companies are only to avoid tax. Those structures were created many years ago by a few assessees to mitigate estate duty and a high wealth tax. Indeed, many have moved to unravel those structures.

If the tax laws on liquidation or deemed dividend are liberalised (even for a limited period of three years), most of these structures would be dismantled.

The author is the Managing Partner of S S Kothari Mehta & Co