This article was first published 15 years ago

Home »

Business » RBI to infuse Rs 480 bn; raps govt for cash crunch

RBI to infuse Rs 480 bn; raps govt for cash crunch

Last updated on: December 16, 2010 14:28 IST

Image: Reserve Bank of India headquarters in Mumbai.

Photographs: Reuters.

With the system facing cash crunch due to outgo on account of advance tax payments and busy credit season, the RBI on Thursday announced measures to pump in Rs 48,000 crore (Ra 480 billion) even as it cautioned against inflation.

It said prices still remained a major concern because of rising demand and high global commodity rates. At the same time, the Reserve Bank kept short-term lending and borrowing rates (repo and reverse repo) as well as mandatory deposit requirement for banks (cash reserve ratio) unchanged.

This is aimed at prompting most banks to hold on to their interest rates. Meanwhile, the market took the announcements with a pinch of salt with the Bombay Stock Exchange's benchmark index Sensex trading lower by over 50 points at 19,594.83 during intra-day trading.

Besides, the rate sensitive sectors like banking, realty were mixed with Bankex trading 0.47 per cent higher and Realty index at 0.03 per cent down.

The RBI measures came on a day when food inflation rose to 9.46 per cent for the week ended December four from 8.60 per cent a week ago, and the central bank also did not rule out the possibility of the rate of overall price rise going above its projections of 5.5 per cent by March-end.

Hike in petrol prices is also expected to add to inflationary pressures. However, overall inflation has been declining persistently and stood at 7.48 per cent in November. Enthused by 8.9 per cent growth rate for the second quarter, RBI, however, did not change its projections of 8.5 per cent economic growth this fiscal and preferred to revisit numbers at its next review on January 25, 2011.

...

Image: Indian currency notes are stapled to form garland at market in Jammu.

Photographs: Mukesh Gupta/Reuters.

Blaming the government's huge cash balance for aggravating liquidity situation, the central bank said it will purchase sovereign securities for Rs 48,000 crore in a month, expected to ease situation of cash-strapped system a bit.

It also cut Statutory Liquidity Ratio (SLR), which is a requirement for banks to keep portion of their deposits in government securities, cash and gold, by one percentage point to 24 per cent from the present 25 per cent.

However, the measure is unlikely to provide any immediate relief to the system, as RBI has already announced that it will not penalise the banks even if their SLR comes down two percentage points below the mandatory requirement.

That facility now stands cut to one percentage points, RBI said today. The RBI cautioned that its moves should not be seen as a change in the policy stance, since "inflation continues to remain a major concern."

However, technically RBI's move is a first measure stance this year of a pause on its rising rates spree. The central bank said while it expected liquidity to remain in short supply, "the extent of tightness has been beyond the comfort level of the Reserve Bank."

"This has been mainly due to persistence of large government cash balances which have averaged Rs 84,000 crore since the Second Quarter Review of November," it said.

The government got over Rs one lakh crore from the sale of spectrum to high speed telecom and broadband services against its projections of Rs 35,000 crore in the Budget.

It is also expected to get robust tax collections from corporates in advance payments for third quarter. Bankers said RBI actions would enable most banks to not further raise their interest rates.

Oriental Bank of Commerce Executive Director S C Sinha said, "RBI's action would put on hold deposit rate hike for some time and lending rate hike. The rate hike would come from those banks which have not done in the last one month," he said.

Major banks like ICICI Bank, HDFC Bank, PNB had raised their interest rates, while the country's largest lender, SBI had hiked only deposit rates.

Image: A bank teller counts notes.

Photographs: Reuters.

Chief economic advisor Kaushik Basu said, "There had been concern about liquidity situation. They (RBI) had to do a bit of fine balancing act between the easing liquidity situation and the same time making sure that there isn't greater pressure on interest rates."

The extent of liquidity strain could be gauged from the fact that banks borrow net over Rs 1 lakh crore on an average daily from RBI through its repo window.

The Reserve Bank had also announced recently two rounds of purchase of government securities for Rs 12,000 crore (Rs 120 billion) each through open market operations (OMO). Today's move to inject Rs 48,000 crore will also come through OMO, by which RBI manages liquidity through purchase and sale of government securities.

Even as RBI cautioned that "risk to projection of 5.5 per cent inflation by March 2011 is on the upside,", the Finance Ministry down played concerns on inflation. "They (RBI) have taken a call on the fact that inflation has moderated and the basic problem today, though temporary, is liquidity deficit", Finance Secretary Ashok Chawla said.

"So, they have responded to that which will make Rs 48,000 crore available in terms of injection. That is important, very crucial, so that credit delivery is not impacted," Chawla said.

The Reserve Bank, however, said though inflation has moderated, inflationary pressures persist both from domestic demand and higher commodity prices. "The pace of decline in food price inflation has been slower than expected due largely to structural factors.

There is a risk that rising international commodity prices will spill over into domestic inflation," the central bank said. Global oil prices are ruling at 88.55 dollars a barrel, despite moderation. Freezing winters in Europe will also add further pressure on oil prices. In India, petrol prices were recently hiked by close to Rs 3 a litre.

RBI also said, "Going forward, rising domestic input costs for the manufacturing sector combined with aggregate demand pressures could weigh on domestic inflation." Industry, which was critical of RBI's earlier actions of raising policy rates, said it is "extremely delighted" with the central bank's action to halt hike in key rates and address the liquidity problem.

Click NEXT to read RBI's outlook on the global economy, inflation and liquidity...

Image: A slow recovery.

Global Economy A slow recovery and persistent unemployment motivated another round of quantitative easing in the US.

However, recent data show some signs of improvement, especially in respect of real GDP and consumer confidence, even though the unemployment rate has increased.

Although economic recovery has been progressing in Europe, financial stability concerns have resurfaced as the sovereign debt problem spread further. Major emerging market economies (EMEs) continue to experience robust growth.

Significantly, despite the slow recovery and slack capacity in advanced economies, international commodity prices such as oil, food, industrial inputs and metals have risen noticeably in recent weeks. Reflecting the strength of demand and higher commodity prices, inflation has started creeping up in most EMEs.

Image: Farmers sit beside heaps of wheat at a grain market in Chandigarh.

Photographs: Ajay Verma/Reuters.

GDP Growth A GDP growth of 8.9 per cent in Q2 of 2010-11 suggests that domestic momentum remains strong. Agricultural growth has recovered on the back of a good monsoon.

After flagging during August-September, the index of industrial production (IIP) grew by over 10 per cent in October 2010. Various indicators of industrial activity, including the Purchasing Managers' Index (PMI) also suggest a strong underlying momentum.

Lead indicators of services sector activity have continued to increase at a robust pace.

These developments reinforce the Reserve Bank's projection of 8.5 per cent for real GDP growth for 2010-11 which will be reviewed in the Third Quarter Review scheduled on January 25, 2011.

Image: Inflation, a concern.

Photographs: Reuters.

Inflation After remaining in double digits for five successive months, year-on-year headline WPI inflation declined to 8.8 per cent in August 2010 and further to 7.5 per cent in November 2010.

Consumer price (CPI) inflation for industrial workers and rural/agricultural labourers softened to single digit rates from August 2010, after remaining in double-digits for over a year.

The overall reduction in inflation reflects moderation of food price inflation following a favourable monsoon.

Food price inflation moderated from an average of 15.7 per cent in Q1 of 2010-11 to 12.3 per cent in Q2, to 10.0 per cent in October 2010 and further to 6.1 per cent in November 2010.

Image: Moderation in inflation for cereals and pulses has been larger.

Photographs: Reuters.

Amongst food items, the moderation in inflation for cereals and pulses has been larger than that in inflation of protein related food items such as egg, fish, meat and milk reflecting the structural nature of food inflation.

In addition, inflation for non-food primary articles such as raw cotton, raw rubber and minerals rose sharply. Reversing the declining trend in the last six months, non-food manufactured products inflation edged up to 5.4 per cent in November 2010.

Though inflation has moderated, inflationary pressures persist both from domestic demand and higher global commodity prices. The pace of decline in food price inflation has been slower than expected due largely to structural factors.

Image: Rising international commodity prices, a concern.

There is a risk that rising international commodity prices will spill over into domestic inflation.

Going forward, rising domestic input costs for the manufacturing sector combined with aggregate demand pressures could weigh on domestic inflation.

The risk to the Reserve Bank's projection of 5.5 per cent inflation by March 2011 is on the upside.

Image: Liquidity deficit.

Liquidity

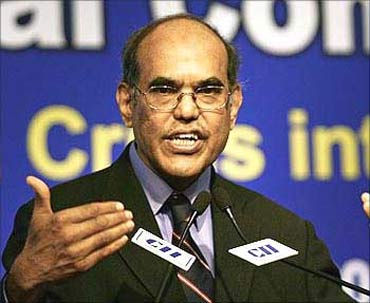

While the overall liquidity in the system has remained in deficit consistent with the policy stance, the extent of tightness has been beyond the comfort level of the Reserve Bank.

This has been mainly due to persistence of large government cash balances which have averaged Rs 84,000 crore (Rs 840 billion) since the Second Quarter Review of November, mirroring in the average net LAF repo amount of Rs 1,01,000 crore (Rs 1.01 trillion).

In addition, the liquidity deficit has been accentuated by structural factors such as significantly above-trend currency expansion and relatively sluggish growth in bank deposits even as the credit growth accelerated in 2010-11.

Image: RBI Governor D Subbarao.

Photographs: Reuters.

While the liquidity deficit improved transmission of monetary policy signals with several banks raising deposit and lending interest rates, excessive deficits induce unpredictability in both availability and cost of funds, making it difficult for the banking system to sustain credit delivery.

In view of the persistent liquidity pressures in November 2010, the Reserve Bank implemented some measures such as additional liquidity support to SCBs under the LAF up to 2.0 per cent of their NDTL, continuation of second LAF, and OMO purchase of government securities.

Image: More liquidity to help economy.

While these measures have helped stabilise overnight interest rates, the extent of deficit could constrain banks' ability to expand their balance sheets commensurate with the productive needs of the economy.

The additional liquidity measures initiated by the Reserve Bank respond to these concerns.

As the economy expands, it needs primary liquidity, which will have to be provided in a manner consistent with the monetary policy stance.

Such provision of liquidity should not be construed as a change in the monetary policy stance since inflation continues to remain a major concern. The measures taken in this review need to be appreciated in that context.

Source:

PTI© Copyright 2026 PTI. All rights reserved. Republication or redistribution of PTI content, including by framing or similar means, is expressly prohibited without the prior written consent.