On the face of it, the December 2013 quarter has been the best for India Inc in three years.

Net profit for 3,107 non-financial and oil & gas companies was up nearly 25 per cent over the corresponding quarter a year ago.

This is a smart turnaround, considering the same set of companies reported a decline in earnings growth in the previous four quarters.

But dig deeper and the shine comes off. Demand growth in the domestic sector remains anaemic and the boost in earnings is largely due to a good show by companies in defensive (consumer staples) and export-oriented sectors such as pharma and information technology services.

“Volume growth across sectors decelerated and non-performing loans remained high in the third quarter, reflecting a slowdown in the economy,” say analysts led by Sanjeev Prasad in a recent report by Kotak Institutional Equity.

. . .

The combined net sales for non-oil and financials companies was up 9.9 per cent.

Adjusted for double-digit consumer inflation it signals flat- to-negative volume growth.

Revenue growth falls to 8.1 per cent if fast-moving consumer goods, IT and pharma companies are excluded, indicating stress in the economy.

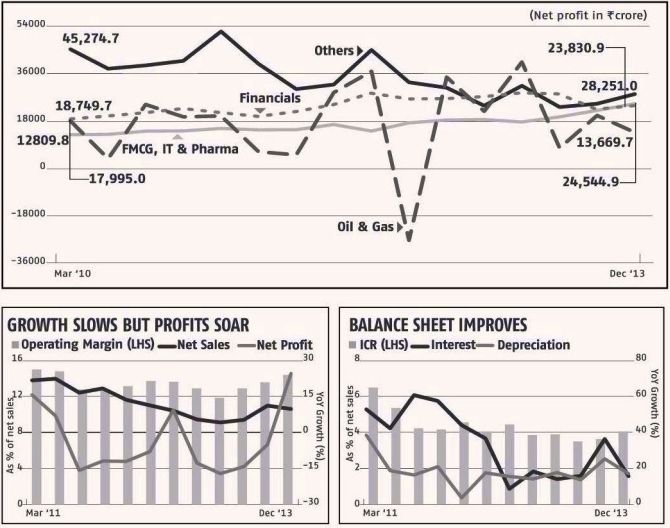

The impact of defensive companies on India Inc’s profitability is even bigger.

The combined net profit for defensives was up 33 per cent, the most in three years.

In comparison, others reported 18.7 per cent growth in net profit, while bank & financials (- 12.5 per cent) and oil & gas (- 37 per cent) companies saw a dip in profits in the third quarter.

Not surprisingly, the benchmark indices are now largely driven by defensives.

. . .

In the past four years (16 quarters), the combined net profit of defensives has nearly doubled, while others reported a 38 per decline in profits.

FMCG, IT and pharma companies now account for 47.5 per cent of the net profit of all non-oil and financial companies, up from 22 per cent four years ago (see chart).

A similar trend is visible in the performance of India’s top 50 companies that are part of the National Stock Exchange’s Nifty index.

According to a study by Emkay Global Financial Services, the combined revenues of 16 Nifty companies with forex exposure was up 19.1 per cent year-on-year in the quarter, against 7.8 per cent growth reported by others.

The combined revenues for all Nifty companies were up 16 per cent in the quarter.

. . .

Nifty companies’ net profit shows an even stronger co-relation with currency movement.

Net profit for dollar-denominated companies (those with forex exposure) was up 34.4 per cent, against 6.7 per cent growth reported by others.

Overall, Nifty companies’ combined earnings rose 17 per cent in the third quarter over the corresponding period last year.

“The impact of rupee depreciation has been stronger than anticipated.

“It boosted export volumes and cushioned the blow from the domestic slowdown somewhat, besides expanding margins,” says Dhananjay Sinha, head institutional research at Emkay Global Financial Services.

In the normal course, the rupee depreciation should have negatively impacted profit margins through higher rupee prices for energy and raw materials such as metals and petro-chemicals.

. . .

Higher subsidies on fuel, food and fertilisers, however, insulated domestic prices from currency depreciation.

The result was a 150-basis-point increase in core operating margins (excluding the impact of other income) for non-oil and financial companies.

While operating margins in pharma and IT companies touched a four-year high, even FMCG, auto, metals, consumer durables and capital goods reported higher margins, thanks to favourable exchange rate.

This has raised the prospect of a dip in margins once the impact of the rupee depreciation begins to fade beginning the June ’14 quarter, and the new government that will take charge in could cuts subsidies.

This may explain why the stock market remained cool to the results and indices continue to be range-bound.

. . .

Others, however, expect IT and pharma companies to maintain their momentum, given the strong order pipeline and the economic recovery in US and Europe.

“Most IT companies remained bullish about the demand prospects and are likely to retain their earnings momentum in the next financial year as well,” says Nitin Jain, head, capital markets at Edelweiss Capital.

His biggest worry is the continued stress in banking and financials and the demand slowdown in rural areas.

“Demand slowdown seems to have spread to rural areas, with FMCG companies reporting lower volume growth and NBFCs reporting a rise in non-performing assets,” adds Jain.

On the positive side, many analysts see initial signs of a revival in the capex cycle, with an uptick in the order book for capital goods makers.

. . .

“Order inflows for seven industrial companies in our sample increased 44 per cent to Rs 39,600 crore (Rs 396 billion).

“We have now seen a few quarters of growth in order inflows, which suggests there is finally some progress in the investment cycle,” says Prasad.

Analysts are advising investors to remain stock-specific with a bias towards top names in defensives and export-driven sectors such as IT and pharma.

They are still reluctant to recommend cyclical stocks such as capital goods makers and construction firms despite their low valuations, given the challenges in reviving the capex cycle.

The only exceptions are top private sector banks and select NBFCs with exposure to housing loans.