Second-tier NBFC stocks are trading at 24.4x their trailing earnings, which is nearly twice their 15-year average of 13.9x

A sharp decline in share prices of non-banking finance companies (NBFCs) on Friday is forcing some analysts to ask the obvious question: Was the correction overdue, given the sector’s rich valuation despite the steady rise in bond yields, which is set to raise lenders’ cost of funds, adversely affecting their margins?

The country's top retail NBFCs are trading at 23.5 times their trailing 12-months earnings nearly 500 basis points higher than the sector's 15-year average price to earnings multiple of 18.4 times.

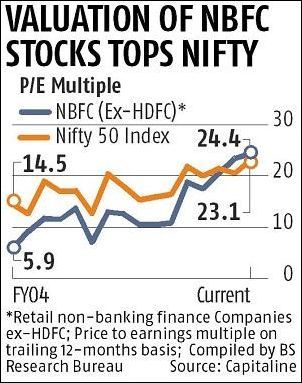

Top non-bank lenders are also trading at a premium to the underlying valuation of the benchmark Nifty 50 index against a discount historically. (See the adjoining chart)

Top non-bank lenders are also trading at a premium to the underlying valuation of the benchmark Nifty 50 index against a discount historically. (See the adjoining chart)

The valuation rerating is even higher in the second tier (excluding Housing Development Finance Corporation) stocks in the sectors.

Second-tier NBFCs are trading at 24.4x times their trailing earnings, nearly twice their 15-year average P/E multiple of 13.9x.

Many of these stocks are also trading at a premium to both the benchmark index and HDFC, the sector's bellwether.

HDFC is the largest non-bank lender in the country, accounting for nearly half the industry's revenues, profits and market capitalisation, despite an erosion in its market share in recent years.

Historically, the lender has always traded at a premium to the broader market valuation due to its superior balance sheet ratios.

"Retail NBFCs got a tailwind from a sharp decline in the interest rates beginning second half of 2014 and growth opportunity opened by the inability of public sector banks to make incremental lending due to bad loans.

"The tailwinds have now weakened, as interest rates are rising and banks have become aggressive in pushing retail loans," says G Chokkalingam, founder and MD, Equinomics Research & Advisory Services.

The analysis is based on the annual financials of 13 retail NBFCs, whose numbers are available for last 15 years.

The sample includes HDFC, LIC Housing, Shriram Transport Finance and Bajaj Finance among others.

The average cost of funds for retail NBFCs declined by nearly 190 basis points from a high of 10 per cent in FY2012-13 to 8.1 per cent during FY18.

The decline was even sharper for lenders ex-HDFC. Their average cost of borrowing declined to 8.5 per cent in FY18 from an average of 10.5 per cent in FY13.

The yields on 10-year government of India bond declined from high of 9.5 per cent in last quarter of 2013 to record low of 6.5 per cent in the last quarter of 2016.

The bond yields have since crossed 8 per cent putting upward pressure on NBFCs’ cost of borrowings.

Analysts said that the banks have an advantage over NBFCs in the high interest rate scenario due to their low cost of funds.

"Access to low cost saving and current account deposits offers cost advantage to commercial banks over NBFCs which borrow from the open market," says Dhananjay Sinha, head of research, Emkay Global Financial Services.

This is especially true for smaller NBFCs, which have to pay higher interests rates to borrow through bond market compared to large and top rated NBFCs such as HDFC.

Analysts also say that NBFCs are also likely to face funding pressure from decline in fund flow in mutual funds in recent quarters.

“There was a surge in mutual fund investments by high net worth individuals and businessmen post note-ban in 2016 and trade disruption caused by goods and services tax.

"This was largely invested in NBFC papers. Now the fund flow is reversing making it tough and expensive for NBFCs to make incremental borrowings,” says Dhananjay Sinha.

This is likely to force many lenders to go slow on loan growth besides eating into their margins and profitability leading to a de-rating of their valuation.

Photograph: Reuters