The expansion in equity market volumes is driven by retail speculators indulging in heavy trading of complex derivatives that are economically unproductive, say Praveen Chakravarthy and T V Somanathan.

The expansion in equity market volumes is driven by retail speculators indulging in heavy trading of complex derivatives that are economically unproductive, say Praveen Chakravarthy and T V Somanathan.

India is one of the most successful countries in developing a vibrant securities markets which reiterates the strengths of modern development in India's capital markets.’

This is a justifiably proud proclamation by the National Stock Exchange in its annual report of 2013. The value of equity trading volumes on India's two major stock exchanges, BSe and NSE, combined has increased nearly 50 times between April 2002 and March 2014. NSE has risen to rank in the world's top two exchanges in terms of number of trades. Yet, this is perhaps a Pyrrhic victory for the Indian equity markets. Ninety-six per cent of this multi-fold expansion in equity market volumes is driven by retail speculators indulging in heavy trading of complex derivatives that are perilous and economically unproductive.

Ever since the Dutch East India Company issued shares to the general public in 1602 to raise capital to build the spice trade, the primary and sacrosanct role of a stock market in a nation's economy is to mobilise household savings to raise capital for companies, which then create jobs and provide impetus to economic growth. The supplementary objective of a stock market, to act as an efficient price discovery mechanism and provide liquidity in trading of shares through its secondary markets, is integral to its primary objective.

Casting aside former US Federal Reserve chairman Paul Volcker’s assertion that the only ever useful financial innovation is the ATM machine, modern finance has popularised derivatives as a tool to hedge risks on future prices of stocks, currencies and commodities. Derivatives form the "tertiary" market, mainly for sophisticated investors and provide liquidity through "fractional margins".

Trading data of the Indian capital markets give the impression that the average Indian investor is extremely sophisticated with an insatiable need to hedge her market risk on a daily basis using complex derivative products. Derivatives trading volumes were 15 times larger than share trading in FY13. In FY13, the value of derivatives trading was 30 times the amount invested directly in companies and government bonds through primary offerings.

According to NSE data, 83 to 87 per cent of all derivatives trading (by value) is by retail investors and proprietary traders, while sophisticated institutional investors account for a mere 13 to 17 per cent. As shown in the chart on the left, ‘Perilous climb’, derivative trading volumes have risen every year since 2001 when they were officially introduced by the stock exchanges and, consistently, retail investors have accounted for 80 to 90 per cent of such volumes every year.

According to NSE data, 83 to 87 per cent of all derivatives trading (by value) is by retail investors and proprietary traders, while sophisticated institutional investors account for a mere 13 to 17 per cent. As shown in the chart on the left, ‘Perilous climb’, derivative trading volumes have risen every year since 2001 when they were officially introduced by the stock exchanges and, consistently, retail investors have accounted for 80 to 90 per cent of such volumes every year.

The structure of India's equity markets can be summed up thus: derivatives worth a trading value of $8 trillion in FY14, largely driven by individual investors and proprietary traders, vis-à-vis less than $200 billion of all forms of capital-raising including government borrowings through bond issues. Derivatives, at best an efficient hedging tool for sophisticated investors and at worst a casino, have catapulted Indian exchanges to the top of the world.

Individual investors indulging heavily in such risky trading of derivatives is akin to regular drivers choosing to drive on racetracks alongside experienced racers. Either these regular drivers are unaware of the risks of racing or incentivised to race or mindless of potentially dire accidental consequences. Irrespective of this, it is undesirable and perhaps unwarranted.

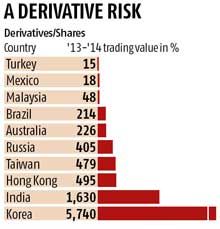

While we acknowledge that the numbers across these three categories are not strictly comparable since derivatives volumes capture notional value and high churn, derivatives trading ratio to shares trading in India is inordinately larger compared to international markets, as evidenced in the table below left, ‘A derivative risk’. Korea, which is the only other market in the world where derivatives trading is significantly higher than shares, sought to address this in 2012 and again in 2014 by increasing the minimum investment size of derivatives to wean small investors out. India ranked third in the world in equity derivatives trading value, but 17th in share trading, in 2012.

An extraordinarily large derivatives market driven by small individual speculators creates an adverse selection problem in terms of the type of new investors it attracts. Investors choosing to bet on the direction of stock prices with small amounts of money tend to only attract other speculators and operators into the market. Price manipulation and rumour-mongering are the risks of such a market. This makes the overall market more speculative in character, leading to a trust deficit and runs the risk of scaring away longer-term investors.

An extraordinarily large derivatives market driven by small individual speculators creates an adverse selection problem in terms of the type of new investors it attracts. Investors choosing to bet on the direction of stock prices with small amounts of money tend to only attract other speculators and operators into the market. Price manipulation and rumour-mongering are the risks of such a market. This makes the overall market more speculative in character, leading to a trust deficit and runs the risk of scaring away longer-term investors.

This is perhaps already reflected in the Securities and Exchange Board of India's investor surveys, where a lack of trust in the equity markets is the single-biggest reason cited by households for not investing more in equities.

There is no documented survey that explains the choice of derivatives for retail investors but transaction tax arbitrage between trading in shares vis-à-vis derivatives is one plausible explanation. The other is the small size of contracts and availability of margins for derivatives trading that amplify investment positions versus a similar amount invested in shares directly.

Systemic risks and costs of a high percentage of retail investors in speculative trading through complex derivatives are very high. The risk is one of a catastrophic economic loss for retail investors due to leveraged positions in derivatives, where the potential loss may be unlimited and further eroding trust in the markets. The costs are domestic capital being diverted away from productive investment.

Economic growth in India, driven primarily by private enterprise, requires large amounts of capital. Channelling India's high household savings to such productive economic purposes is prudent. Appropriate taxation and other policy measures to wean retail investors away from risky, unproductive derivatives, to investing in primary and secondary markets will augur well and be the harbinger for healthy equity markets.

Praveen Chakravarty is a former CEO of an investment bank and a member of corporate boards and policy committees. T V Somanathan is an IAS officer, former joint secretary, ministry of corporate affairs, and author of books on derivatives. These views are personal.